Navigating Rates

Forget the high yield myths:

rethinking a USD 2.2 trillion market

We think it’s time to forget the myths about high yield fixed income. With a resilient economic outlook and generally robust corporate health, the once-niche segment of financial markets has grown to more than USD 2.2 trillion. High yield is becoming an integral part of fixed income portfolios, providing a useful source of return and diversification.

Key takeaways

- High yield bonds can play an important role in boosting a portfolio’s return potential, demonstrating an ability to outperform other fixed income segments over the longer term. High yield returns tend to have relatively low correlations with other asset classes, allowing diversification benefits.

- A relatively stable economic outlook, strong fundamentals of companies and a record level of bond proceeds used to refinance existing debt are factors that we think bode well for high yield.

- We think allocating to a global rather than a regional high yield strategy could provide more scope to outperform the broad market and produce a well-diversified portfolio.

The thought of investing in sub-investment grade bonds may seem off-putting to some. However, although high yield is at the riskier end of the fixed income spectrum, the reward is higher potential returns than investment grade bonds and increased portfolio diversification. And we think the current benign outlook for the global economy provides a supportive backdrop. In our view, investing in the asset class globally, rather than on a regional basis, can help to fine-tune performance, taking advantage of regional differences and managing risks in case economic conditions worsen.

Here we challenge four myths around high yield and explain why the asset class may be worth considering now.

Myth 1: Rewards don’t justify the risks

Reality: High yield could boost a portfolio’s risk-adjusted return potential

High yield bonds can provide two major benefits in a balanced portfolio. First, they can increase its return potential. The asset class has demonstrated its ability to outperform other segments of the fixed income universe over the past 15 years (see Exhibit 1).

Second, their ability to diversify a broad asset allocation. That’s because their returns tend to have relatively low correlations with US Treasuries, one of the biggest components of the fixed income universe. This means an allocation to global high yield can improve a portfolio’s risk-adjusted return potential.

Exhibit 1: Global high yield returns have outperformed other fixed income segments since 2009

Source: ICE indices, Bloomberg, cumulative monthly total returns from 31/08/2009 to 31/08/2024. Past performance does not predict future returns.

Myth 2: Companies within the high yield universe are more likely to default

Reality: Firms are issuing bonds to refinance their existing debt, which bodes well for default rates

Investors who aren’t sure whether to allocate to high yield often cite the potential for defaults as one of their biggest concerns about the asset class. But we believe default rates shouldn’t be a major cause for concern at present. Indeed, the current environment should be supportive of high yield. The IMF recently upgraded its growth forecast for the US economy. A stable economy with a resilient growth outlook can reduce the risk of companies getting into financial trouble.

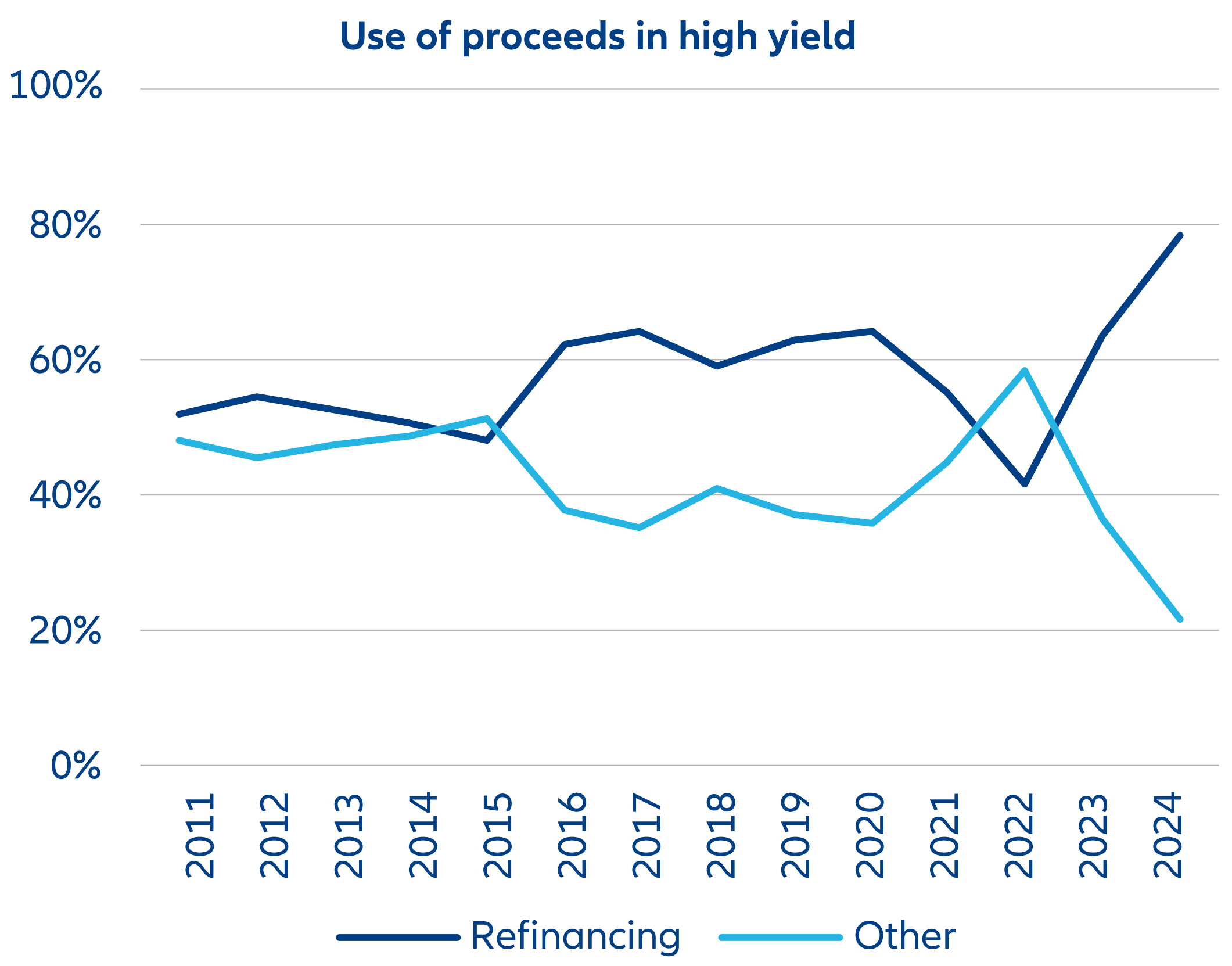

A measure we follow that helps gauge the creditworthiness of the high yield market is use of proceeds – in other words, what the money raised by issuing high yield bonds is to be used for. It can be used for two main purposes. The first is refinancing, which extends the maturity wall – the period when a significant amount of debt is due – and reduces the risk of a company defaulting. The second is general business operations, M&A and paying dividends. Refinancing falling below 50% of total new issuance is a sign that leverage is increasing in the market and that default rates could rise. But the proportion of proceeds being used for refinancing has hit a record high in 2024 (see Exhibit 2), which bodes well for default rates.

Exhibit 2: The proportion of proceeds being used by high yield issuers for refinancing has hit a record high in 2024

Source: Allianz Global Investors and LCD Pitchbook, July 2024. Past performance does not predict future returns.

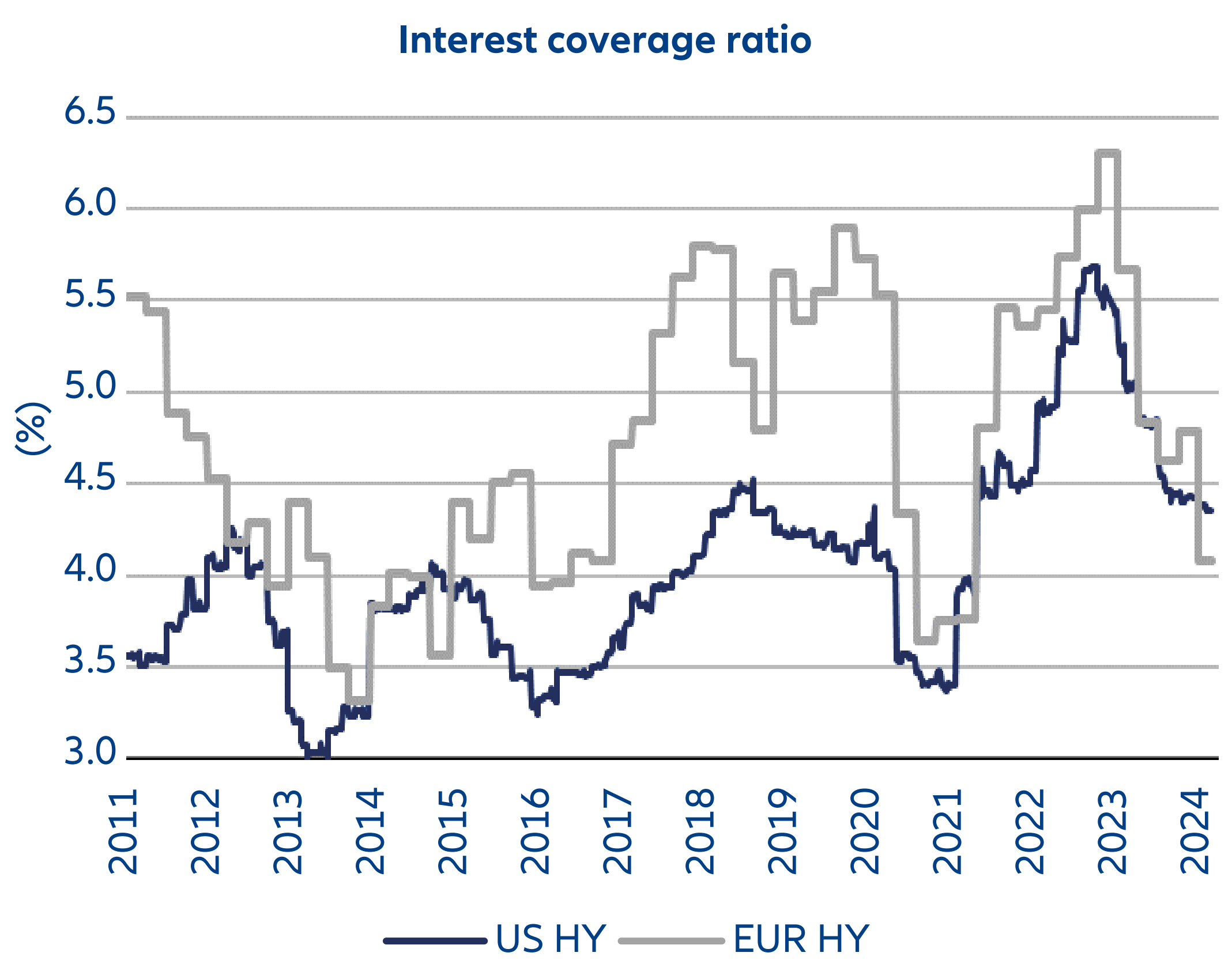

It’s also worth noting that the interest coverage ratio (showing how easily a company can pay off its debt) while dropping as cheap financing is being replaced by borrowing at higher rates, remains well above 3 (see Exhibit 3), the level below which analysts typically begin to become concerned about companies’ ability to pay.

Exhibit 3: High yield’s interest coverage ratio remains stable

Source: BofA Global Research, July 2024. Past performance does not predict future returns.

Myth 3: High yield issuers are small players in niche sectors

Reality: The high yield universe is increasingly made up of large companies

The high yield market’s strong growth has provided a wide range of companies with improved access to the capital they need to grow. This has been particularly beneficial for small- and medium-sized enterprises that do not qualify for investment grade ratings.

But the high yield market has faced competition as a source of financing from the growth of private debt in recent years. Small-cap companies and firms in niche sectors like technology and biotech are among the firms turning to private debt. As a result, high yield is now financing larger businesses that are often less niche than in the past.

According to Bank of America, US high yield issuers have average earnings of around USD 1.2 billion – well above the average of around USD 500 million since the global financial crisis. By way of comparison, US investment grade companies’ earnings average around USD 2.2 billion, having ranged between USD 1.5–2 billion over the past 20 years. In other words, 20 years ago the average US high yield company was around 25-30% the size of the average investment grade company, but today it is over half the size.

This is important because larger companies generally have more levers to pull if they enter financial distress, which may be one reason why default rates have been lower since the global financial crisis.

Myth 4: Investing in a regional high yield market can be an effective starting point

Reality: Investing in high yield on a global basis provides more scope to outperform and produce a diversified portfolio

Many investors in high yield choose to access the asset class by investing in a US or euro high yield strategy, or both. But we believe allocating to a global strategy could provide more benefits.

A regional approach typically invests only in companies from one region issuing primarily in one currency. The manager seeks to outperform through sector and security selection and by adapting the portfolio’s beta. A global strategy, by contrast, can generate outperformance from additional sources.

No individual high yield market has consistently posted better returns than the others over time (see Exhibit 4). A global high yield manager can continuously adapt their portfolio’s regional allocation based on changes in the prevailing backdrop to maximise its return potential. This is very different from adopting a static allocation to regional buckets.

Exhibit 4: No individual high yield market has consistently performed better than others over time

Source: Allianz Global Investors, Bloomberg, ICE Bank of America Merrill Lynch, as of 31/03/2024. Past performance does not predict future returns.

What’s more, they can exploit regional growth differences by, for example, allocating to cyclical sectors in regions whose economies are growing most strongly and to defensive sectors in regions whose economies are struggling. Current regional economic divergence affords the opportunity to put such an approach into practice. Growth in the US is set to outperform most other parts of the developed in 2024 and 2025, while growth in Europe and Japan will be more sluggish.

We acknowledge that spreads between high yield bonds and US Treasuries are tight on a global basis, reflecting investor belief that the outlook for companies is positive. In our view, the spread remains attractive in the context of still solid economic growth in the US and a robust outlook for companies. But we think caution is warranted in case the outlook worsens.

A global manager can help to navigate a shifting landscape, capitalising on spread, currency and interest rate differences between regions. For example, the current environment may require shifting greater allocation to benefit from wider spreads in European high yield and higher credit quality in comparison to the US market.

From a bottom-up perspective, a global strategy will have a significantly broader range of issues to invest in within each sector, and there will also be opportunities in different currencies. The approach offers potential for diversification – a fundamental pillar of any investment portfolio.

Find out more about high yield: Global high yield: the investment case for a growing asset class