The China Briefing

Putting cash to work

Please find below our latest thoughts on China:

- China’s markets have paused for breath after the hectic rally in recent months. The largest China stock by market capitalisation, Tencent, is up by more than 100% since the low point at the end of October last year.1

- Recent days have seen some profit taking in offshore China in particular. As a result, there has been some catch-up in the relative performance of China A-shares. Year to date, the MSCI China A Onshore Index is now ahead of MSCI China.2

- Part of the reason for the market lull is because there has been a relative news vacuum. This won’t last for long, however.

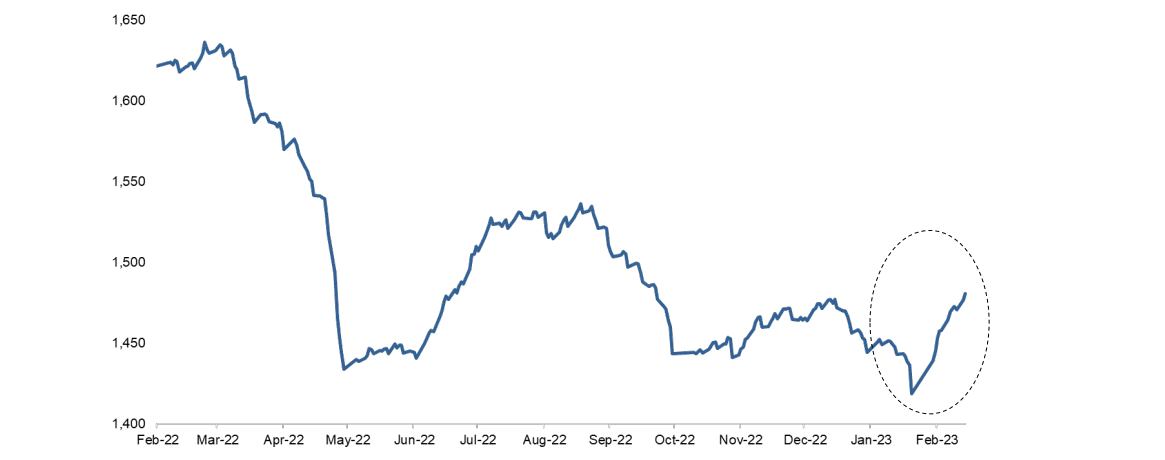

Chart 1: Margin trading outstanding balance in China A-Shares (CNY billion)

Source: Wind as at 14 February 2023

- The next results season gets underway in earnest in a few weeks. The results themselves are likely to be very weak, reflecting the early stages of the reopening when Covid was spreading rapidly and many people isolated at home. More interesting will be to hear what companies are saying about early signs of business recovery.

- Also coming up on 5 March is the so-called “Two Sessions”, the joint annual meetings of China’s national legislature and the top political advisory body.

- The event carries particular significance this year for two main reasons. The first is that all new political appointments will be confirmed, a process which started almost six months ago at the Party Congress. With the heads of key departments in place, policy implementation should be accelerated.

- The second area of significance relates to the 2023 GDP growth target – expected to be at least 5% – and more details on policy support to achieve the target. Having undershot last year, officials will no doubt be incentivised to over-achieve their KPIs this time around.

- The rumour mills are in full swing with expectations of consumption coupons for smaller cities, more fiscal stimulus on infrastructure projects and potentially higher leverage in state-owned enterprises (SOEs) to provide additional domestic demand.

- One notable economic data point recently was the robust monthly new credit data for January, which came in significantly ahead of expectations and was the second-highest level on record. Banks have clearly been following the regulator’s instructions to step up lending.

- We continue to expect a significant economic recovery in coming months, with the services sector leading the way.

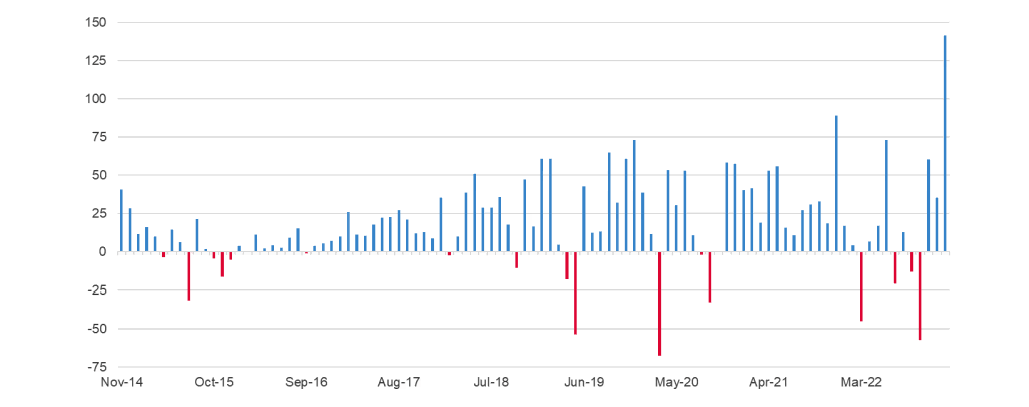

Chart 2: Monthly northbound net buying / selling through Stock Connect (RMB bn)

Source: Wind, Allianz Global Investors, as at 31 January 2023.

- Over the past three years, the shape of China’s growth has changed dramatically. As a result of Covid restrictions, the contribution of the service sector to GDP growth fell from 63.5% in 2019 to just 42% in 2022, 3 reversing a multi-decade trend.

- In contrast, the contribution of the secondary sector (mining, manufacturing, utilities and construction) increased to 47.7% from 32.6% in 2022, 4 on the back of booming export demand and infrastructure investment.

- We believe that this growth pattern is likely to reverse in 2023 now that Covid constraints are removed. And as consumer confidence returns, this could also act as a catalyst for households to put high levels of cash to work.

- Household bank deposits in China increased by a record RMB 17.9 trillion (approx. USD 2.6 trillion) in 2022.5 To put that into context, this increase alone is equivalent to around 60% of Germany’s GDP and over 80% of the UK’s GDP. 6

- The massive increase in deposits suggests there are excess savings waiting to be spent or invested, a development that has helped to underpin the renewed bullishness on China’s growth outlook and asset prices.

- Indeed, there have been signs recently of improving domestic investor sentiment. The outstanding balance of margin trading in China A-shares, for example, has picked up notably since Chinese New Year.

- And foreign investors have also continued to be buyers. Year to date, there has been around USD 22 billion of net buying through the northbound Stock Connect into China A-shares. This is already well ahead of the whole of 2022 (USD 13 billion).7

1 Source: Bloomberg as at 15 Feb 2023

2 Source: Bloomberg as at 15 Feb 2023

3 Source: Bloomberg, Gavekal, 13 Feb 2023

4 Source: Bloomberg, Gavekal, 13 Feb 2023

5 Source: Gavekal, 1 Feb 2023

6 Source: World Bank, 2023

7 Source: Wind, 14 Feb 2023