The China Briefing

Go with the flow

China equities rebound as tech and AI thrive, retail investors return, US-China relations stabilize, and policy boosts market confidence amid excess savings shifts.

Please find below our latest thoughts on China:

- As one chapter closes, another opens. China property company Evergrande was delisted from the Hong Kong stock exchange on Monday. It marks a spectacular collapse having once been valued at more than USD 50 billion.1

- Although China’s housing market continues to be weak, its impact on the country’s financial markets has been lessening for some time.

- Credit markets bottomed almost two years ago.2 It’s taken a lot longer – and several false dawns – for confidence in equities to rebuild. But the breakout in recent weeks, supported by record trading volume3, suggests that China equities have finally turned the corner.

Chart 1: Performance of China equities since June 2024 (USD, rebased to 100)

Source: LSEG Datastream, Allianz Global Investors, as of 22 August 2025.

- While the macro story is still challenging, there are nonetheless some encouraging fundamental factors supporting the market rally.

- Much of the market strength has been focused on the tech sector. While DeepSeek was the high-profile catalyst earlier this year, much of the groundwork for China’s AI surge has been laid for over a decade.

- In 2017, the government established AI as a national strategic focus, prioritising computing infrastructure, AI chips and cloud services.

- Supported by a vast pool of STEM (science, technology, engineering and maths) talent, extensive data centre infrastructure, abundant and low-cost electricity and substantial capital, China came to have the ingredients needed for an AI boom.

- Another reason for the positive market sentiment is linked to geopolitics, and the turn of events since the US and China traded ever-higher tariff numbers post “Liberation Day”.

- China’s control of processed rare earth minerals has subsequently provided powerful negotiating leverage, forcing the US to agree to a tariff truce and reversing its previous ban on exports of high-spec AI chips.

- For the time being, at least, US-China relations appear to have found a floor and previous concerns about a sharp slowdown in China’s exports to the US have eased.

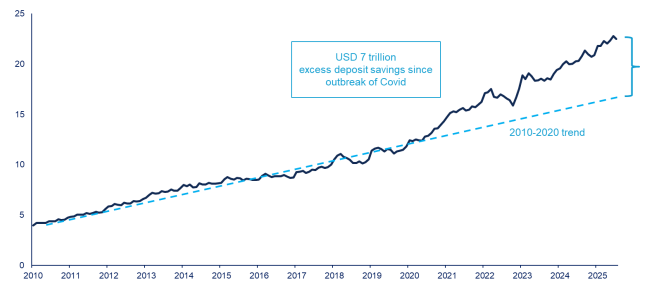

Chart 2: Household bank deposits in mainland China (USD trillion)

Source: Wind, HSBC, Allianz Global Investors, as of 31 July 2025.

- Reviving stock markets has also been a key policy focus for Beijing over the last 18 months or so, since the significant selloff in February 2024.

- Most evident has been the “national team” stepping in to stabilise the China A market during bouts of weakness, sending a strong message about limiting downside risk.

- Other structural changes are also cushioning volatility. The People’s Bank of China is facilitating share buybacks through a new relending programme. And insurance companies are being encouraged to allocate more of their annual premiums into equities.

- While all these factors have played their part in providing the foundation for the market upturn, the most notable short-term change has been the return of China’s retail investors, who until recently have largely stayed on the sidelines.

- Bank deposits have been ballooning for several years reflecting the macro weakness, increased job uncertainty, and the decline in house prices.

- Households in China used to save around USD 1 trillion a year in aggregate, but that roughly doubled during and since Covid. As a result, there are around USD 7 trillion of “excess savings”. That’s about half the size of the China A market.4

- With bond yields and deposit rates at significantly lower levels, this looks to be triggering some reallocation into risk assets.

- China margin financing is the highest in 10 years, daily trading volumes for China A-shares have broken through RMB 2 trillion (USD 270 billion)5, and household deposits in July 2025 grew at the slowest year-on-year rate since 2018.6

- While the rapid pace of the recent upturn might prompt some profit taking, with this combination of factors in place our view is to buy the dips, not sell the rally.

1 Source: Bloomberg, 25 August 2025

2 Source: Bloomberg, 25 August 2025

3 Source: JPMorgan, 13 August 2025

4 Source: HSBC, 2 June 20255

5 Source: JPMorgan, 13 August 2025

6 Source: BNP Paribas, 22 August 2025