Navigating Rates

Tariffs: could “liberation day” shackle the global economy?

US President Donald Trump’s “liberation day” has brought a huge ramp-up in tariffs that some investors fear could sink the global economy. We think the economic impact will be significant – shaving at least 1% off global output – and further escalation of the trade conflict would raise the risk of a recession.

Key takeaways

- The Trump administration’s announcement of a 10% universal levy and higher duties on major trading partners is likely to prompt continued market turbulence in the near term and a flight to safe havens such as gold and short-term US government debt.

- Although much depends on the extent the US’s trading partners retaliate, the tariff status quo as of early April will already cause a significant dent to global growth – with the US being one of the hardest hit. Widespread retaliation could trigger a full-blown trade war and – combined with falling business and consumer sentiment – push the global economy into recession.

- Amid choppy market conditions, we favour European stocks (over US markets), the Japanese yen, gold and US Treasuries; with plenty of twists and turns likely ahead in the global trade dispute, we think further opportunities will emerge.

The rollout of new US tariffs – on what US President Donald Trump called “liberation day” – has fuelled concern about the risk of a full-blown trade war derailing the global economy.

Mr Trump on 2 April announced sweeping “reciprocal” tariffs on imports to the US – probably the highest since the 1930s – with a universal levy of 10% and higher duties on major trading partners, including China (34%), the European Union (20%) and Japan (24%).

At least some economies are expected to retaliate with their own duties on US imports and potentially on services as well. The US has also unveiled a 25% tariff on all foreign-made cars. The latest announcement follows a 25% tariff on all steel and aluminium imports into the US and up to 25% tariffs on Mexico and Canada.

Equity markets fell in the aftermath of the latest news. The extent of the trade dispute’s negative impact remains unclear and it is important to assess the implications by market. Some countries appear to be relative “winners” of this round – such as Mexico, Canada and India – while others will not have expected such a massive “tariff-hammer” (eg, Switzerland and Japan).

While much depends on the degree to which US trading partners retaliate or initiate negotiations with the Trump administration, the tariff hikes announced and already implemented by the US will put a significant drag on global growth. In the short term, we see continued market turbulence and a flight to assets perceived as safer such as gold and short-term US government debt.

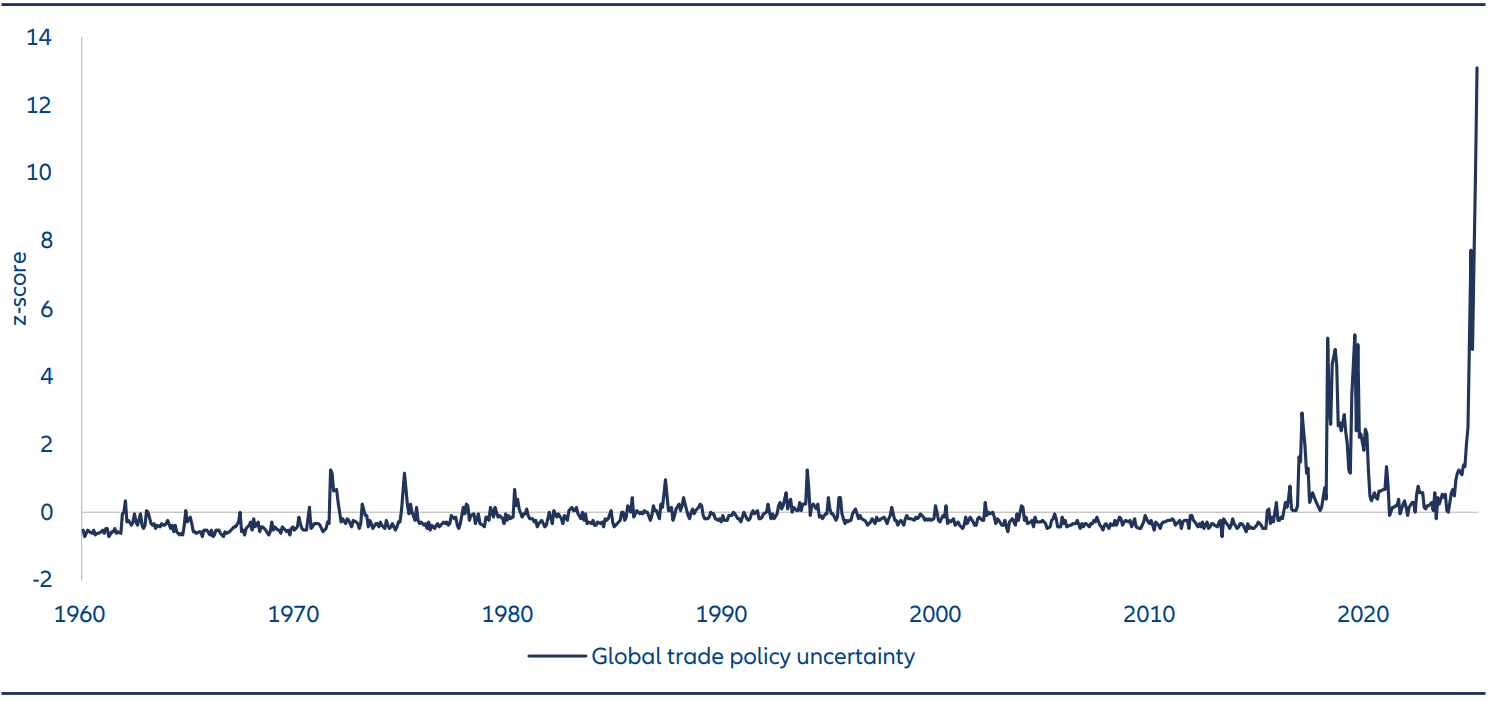

Beyond the direct impact on trade flows, the main transmission mechanism of tariffs is higher trade policy uncertainty (see Exhibit 1), making it more difficult, costly and complex for companies around the world to do and plan business. More complex production chains and a potentially significant administrative burden are key issues that companies will have to navigate in the coming months. The knock-on effect would likely be higher prices of goods and services – lifting inflation – and reduced economic activity

Exhibit 1: Global trade policy uncertainty has reached record highs

Source: Matteo Iacoviello, Trade Policy Uncertainty Index (data as at March 2025).

Full-blown trade war or limited conflict? Two scenarios in scope

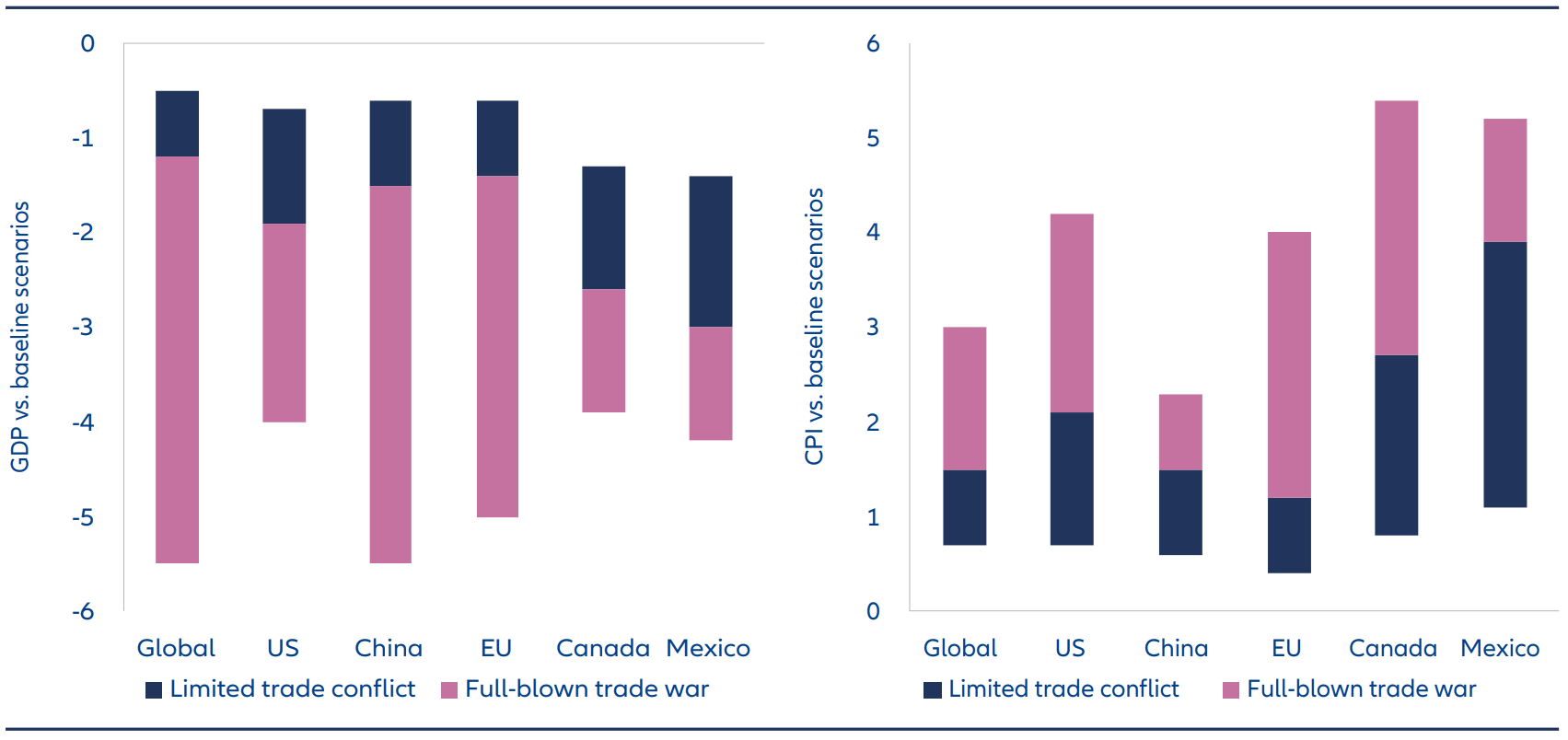

To get more specific, we estimated1 the potential effects on economic growth and consumer price inflation across key affected economies over a one- to three-year period for two scenarios (see Exhibit 2):

- Limited trade conflict: US tariffs rise by 10-25 percentage points (up to 60% on China) with targeted retaliation by affected countries. In this scenario, we assume that, after the initial announcement, negotiations will take place with key partners.

The economic fallout would be significant and further raise downside risks to the global economy. Under these assumptions, the medium-term impact could equate to at least a 1% permanent hit to global GDP and a 0.7% to 1.5% rise in global inflation. Among the economies we assessed, the US would be one of the hardest hit, with growth potentially up to 1.3% lower in the short term.

- Full-blown trade war: US tariffs rise to 60% on China and by as much as 25 percentage points on average on other countries, with widespread retaliation. Combined with an increase in non-tariff barriers, the result would be a deeper economic decoupling between major trading blocs.

A sustained escalation of tariffs and non-tariff barriers (such as import bans or more stringent trade regulations) could drag the global economy into recession within the next year. Our estimates suggest broad-based protectionist measures could reduce US GDP by 2-4%. The downside risk for the global, EU and Chinese economies could be even more severe. In an extreme scenario, global growth would be 1.7-5.5% lower and inflation 1.5-3% higher.

Exhibit 2: Growth and inflation would be worse affected in the event of a full-blown trade war

Source: Allianz Global Investors Global Economics & Strategy, drawing on 29 studies and estimates from multiple sources, including the IMF, OECD, central banks (US Federal Reserve, European Central Bank, Bank of Canada), and private think tanks.

Stagflationary risks loom

Whichever scenario prevails, companies engaged in cross-border trade are operating in a vastly different world than before Mr Trump took office in January. If the Trump administration proceeds with its planned and announced increases, the effective US tariff would surpass even the highest levels of the 1930s, when the then US government introduced wide-ranging protectionist policies via the Smoot-Hawley Tariff Act.

The outlook is further clouded by US policies on immigration (constraining labour supply) and Elon Musk’s drive to improve government efficiency, which involves cutting jobs and other spending. Significantly, these steps have come before any offsetting effect from planned tax cuts and deregulation. Given this backdrop, we have raised our probability of a US recession over the next year to 35-40%.

Even if a recession is avoided, we see an increased likelihood of at least a temporary phase of stagflation, where lower activity and rising price pressures stymy economic growth. We think central banks – especially the US Federal Reserve (Fed) – may be reluctant to cut rates decisively until sustained evidence of weaker growth emerges. This could put it at odds with Mr Trump’s plan to weaken the US dollar and lower interest rates to support the US economy. Based on recent actions, we would not be surprised to see the Trump administration openly criticising the Fed or even putting in place a “shadow Federal Reserve” – a scenario that would certainly be destabilising for financial markets.

Opportunities to consider in a choppy market

In a challenging environment for financial markets, in particular risky assets, we see the following opportunities:

- Favour European versus US stocks: with US stocks bearing the brunt of the recent sell-off in equity markets, we are eyeing opportunities in Europe. The key to performance may be to what extent markets look through US tariffs and focus on the positives such as the fiscal support likely from 2026. Here, the outlook appears more positive and valuations remain relatively cheap and many investors (particularly longer-term institutional investors) remain underweight to the continent’s equity markets. Of course, the impact of tariffs could start to chip away at the region’s competitiveness, but Trump administration policies have served to unify European Union governments. An added tailwind comes from the likelihood of further European Central Bank interest rate cuts whereas we think the US Federal Reserve will halt its rate cuts sooner than expected. If the US sell-off continues unabated, opportunities to capture value may emerge, but for now, Europe has our attention, with a preference for the banking sector.

- The Japanese yen as the US dollar struggles: the US dollar has traditionally benefited from political uncertainties and international investor flows into US assets, such as the Mag 7. But as the once-vaunted band of US tech stocks struggles, so has the dollar. We see the potential for further dollar weakness in light of the trade disputes. Although the US dollar tends to perform well in tail events, the Japanese yen usually does even better and is better armed for negative momentum. Inflation in Japan could easily accelerate, leading the Bank of Japan to raise interest rates later in the summer. With yields on Japanese 10-year government bonds steadily increasing, more of the country’s investors will start repatriating capital, strengthening the yen. A key factor to watch will be the impact a higher yen has on Japanese companies. A sharp appreciation in the currency could hurt Japanese equities, especially with high US tariffs on Japanese imports.

- Gold and US Treasuries as safe haven picks: gold remains our highest conviction call, driven by robust momentum and its role as a hedge against geopolitical risks. It is also reassuring that gold bullion was one of the items exempt from the US tariffs, supporting its tradability. In our view, the yellow metal is a useful diversifier in multi-asset portfolios. Gold prices have hit fresh highs and we think that emerging market central banks and retail investors will boost its value further. US Treasuries are another defensive asset we like. US government debt has benefited from increasing concern about the global economy, outperforming US equities for the first time in five years.

Diversification: adding value in fast-changing market conditions

With plenty of twists and turns likely ahead in the global trade dispute, we think further investment opportunities will emerge in the months to come. As tariffs and non-tariff barriers are hastily announced, enforced and (probably) revised, markets will have only limited visibility about the outlook. We think turbulence will remain a near-term market fixture – and investors could consider trading volatility as an asset class. Derivatives trades in anticipation of the future level of market volatility have historically represented a good hedge against choppiness in equity markets and should also offer re-entering opportunities at a lower cost than beta-one investments in the markets.

In our view, the current uncertainty in markets can play to the strengths of a diversified investment strategy. Building a portfolio that doesn’t rely too heavily on any single asset class or geography may serve investors well in fast-changing market conditions.

1 Drawing on 29 studies and estimates from multiple sources, including the IMF, OECD, central banks (US Federal Reserve, European Central Bank, Bank of Canada), and private think tanks.