Summary

Rising prices for goods and services are one of the biggest risks for investors in conventional government bonds. But there are ways for active managers to generate positive returns from rising – and falling – inflation.

Key takeaways

|

Inflation is one of the main risks that investors in fixed income want to be paid to accept. All else being equal, as the prices of goods and services rise, the same fixed coupon payment buys less of them than it did previously. Rising inflation therefore erodes the real value of fixed nominal cash flows, while rising inflation expectations prompt central banks to tighten financial conditions, influencing the level of yields and the shape of yield curves in fixed income markets. All else being equal, passive bond investors’ return expectations deteriorate when inflation rises.

For active fixed-income investors, however, inflation – like any other risk – can also present opportunities. With the right toolkit and sufficient freedom of manoeuvre, investors can generate positive returns from rising and falling inflation expectations, and from realised inflation that is higher or lower than the market was expecting. The two key questions for investors are, do current risk premia over- or under-compensate for actual inflation risks, and how will inflation expectations change over the period in question?

Providing answers requires us to analyse the four risk premia that combine to produce the yield – not to be confused with the return over a given investment horizon – on a nominal government bond. These are:

- The real risk-free rate: the nominal yield adjusted for the current rate of inflation.

- The real term premium: the extra yield investors demand on longer-dated bonds to compensate them for unexpected changes in economic growth or monetary policy. This is not directly observable but can be modelled.

- The expected inflation rate among market participants.

- The inflation risk premium: the level of compensation that current nominal yields offer for unexpected inflation volatility.

The real yield of a nominal government bond – coupon income, expressed as a yield on the bond’s price, after adjusting for inflation – equals the sum of the real risk-free rate and the real term premium. The sum of the expected inflation rate and the inflation risk premium is usually known as the “break-even inflation rate”. This expresses current market expectations of the average inflation rate over the period in question.

Changing expectations of how these four risk premia will evolve determine the direction of travel for nominal government bond yields. And together these four components – expressed as the real yield plus the break-even inflation rate – combine to form the nominal yield on a government bond.

Having identified the current levels of these four risk premia and decided how we think they will change over a given period, we can turn this view into active positions, whether absolute or relative to a benchmark.

Each of these risk premia can be traded separately, using individual instruments or combinations of them. An active fixed-income manager can therefore generate returns by taking positions either on nominal government bond yields, or on one or several of their risk premia.

Managers can position for falling real government bond yields directly by buying inflation-linked bonds and can use derivatives to position for rising real yields. They can take positions on real term premia via curve trades, in which over- and underweight, or long and short, trades are placed on bonds with different maturities. Positions on the break-even inflation rate can either be relative – by replacing nominal with inflation-linked bonds or vice versa – or outright via inflation swaps. Finally, options on inflation (inflation caps and floors) can be used to hedge out the risk of an unexpected jump (or fall) in inflation. The option price is a measure for the inflation risk premium.

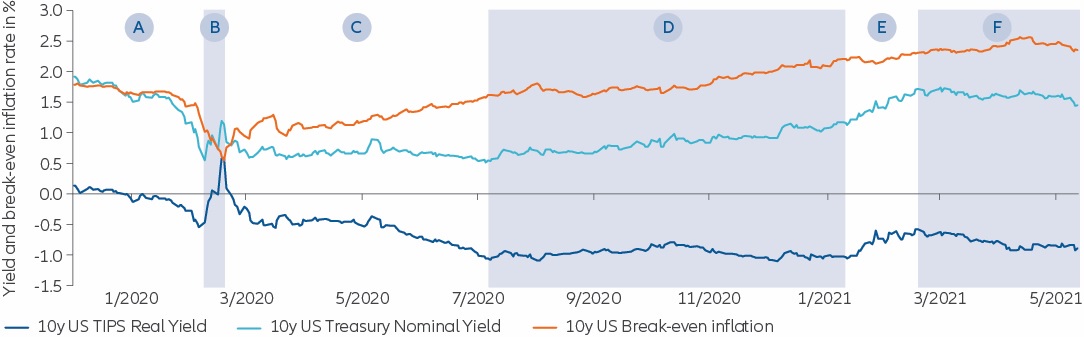

Looking at US long-term bond markets since the beginning of 2020, the graphic shows how the various risk premia have shifted repeatedly over that period. This has led to changes in the market’s view of the outlook for inflation that have required active managers to shift their positioning to generate positive returns.

Chart: 10y US government bond yields (real and nominal) and break-even inflation

See the table below for a closer look at what was driving the changes during each period – and to learn about positioning ideas for different fixed-income instruments

Source: Allianz Global Investors

Market movements and corresponding positioning options to generate alpha

Consult the chart above to see where each period fits into the longer-term comparison of yields and inflation

| Period | Market drivers | Instruments & positioning | |

A01/01/20 – 06/03/20 |

From the second half of February, as growth concerns rose, a flight to “safe-haven” assets led to a collapse of nominal yields and breakevens (as real yields decreased less than nominal yields) | Long nominal government bonds Short inflation via inflation swaps (paying actual inflation, receiving the fixed leg) In relative terms: overweight nominal vs inflation-linked bonds. |

|

B07/03/20 – 19/03/20 |

At the peak of the crisis, investors needed to generate liquidity as quickly as possible, selling the most (and only) liquid parts of their portfolios: government bonds. Real yields rose sharply (much more than nominal yields since TIPS are less liquid and costlier for market makers to hold than nominal government bonds) and breakevens collapsed further. | Short nominal government bond futures Short inflation via inflation swaps (paying actual inflation, receiving the fixed leg) In relative terms: overweight nominal vs inflation-linked bonds. |

|

C20/03/20 – 06/08/20 |

Central banks’ liquidity injections and enormous QE programme announcements calmed markets. Real yields moved back to mid-March levels and then decreased further over the summer towards their low point in early August. Nominal yields decreased only slightly and break-evens rose. | Long inflation-linked bonds Long inflation via inflation swaps (receiving actual inflation, paying the fixed leg) In relative terms: overweight inflation-linked bonds vs nominal bonds. |

|

D07/08/20 – 10/02/21 |

As long-term growth expectations stabilised, real yields moved sideways during the next half year (the term premium rose as shorter-term real yields shrank further on near-term growth fears due to renewed lockdowns). Inflation expectations continued to increase alongside nominal yields. | Long inflation via inflation swaps (receiving

actual inflation, paying the fixed leg) Short nominal government bond futures In relative terms: overweight inflation-linked bonds vs nominal bonds |

|

E11/02/21 – 19/03/21 |

Both real and nominal yields increased markedly between mid-Feb and mid- March. A large part of this move was driven by the real term premium whilst break-even inflation rates rose only slightly. | Short nominal government bond futures Curve trade: short 10y vs long 5y (to benefit from a rising term premium) Long inflation via inflation swaps (receiving actual inflation, paying the fixed leg) In relative terms: overweight inflation-linked bonds vs nominal bonds |

|

F20/03/21 – 11/06/21 |

Both nominal and real yields receded again (moving largely in parallel) whereas break-even inflation expectations went back to mid-March levels. | Long nominal government bonds |

Learn how to turn inflation into an opportunity

Inflation is a key risk for fixed-income investors, but one that active managers can turn into an opportunity. To do so, they must understand and harness the different risk premia that drive government bond yields. Those that do this can generate positive returns from both rising and falling inflation expectations – a critical skill given the uncertain inflation outlook.

Want to view more?

Summary

Many commentators expect the recent rise in inflation to be transitory, but a longer-term reflationary trend – or an increase in inflation expectations – cannot be ruled out. Against this backdrop, private-markets assets have a range of characteristics that could help investors hedge against – and even benefit from – any sustained return to inflation.

Key takeaways

|