Active is: Anticipating what’s ahead

2021 outlook: portfolios need a broader mix as the pandemic prolongs the uncertainty

Summary

While investors can approach 2021 with optimism that an effective Covid-19 vaccine will be available, the path of the economic recovery remains unclear. A broader toolkit of investments is needed – not just the regions, sectors and strategies that have recently done well.

Summary

The recently announced Regional Comprehensive Economic Partnership will likely enhance China’s continued growth story – and will help boost global GDP.

Key takeaways

|

Explore our view on what 2021 has in store

While investors can approach 2021 with optimism that an effective Covid-19 vaccine will be available, the path of the economic recovery remains unclear. A broader toolkit of investments is needed – not just the regions, sectors and strategies that have recently done well.

Key takeaways

- The recovery from the recession sparked by Covid-19 will likely level off in 2021 – but the projected 5% global growth rate could be higher, depending on whether promising new vaccines are successful globally

- Given the massive amounts of monetary and fiscal stimulus, investors will feel side effects – notably high valuations in several major asset classes – emphasising the need for careful selection among securities and regions

- In an uncertain equity market, seek overall balance: equities in Europe and Asia may provide better value than the US winners of 2020, and value stocks may begin to catch up with growth stocks

- The Covid-19 pandemic reinforced the importance of sustainable investing; public/private partnerships, a focus on impact investing and alignment with the UN’s Sustainable Development Goals can help investors achieve meaningful real-life change as countries address vital environmental and economic development issues

- Longer-term US government bonds may be less attractive if the yield curve steepens as expected; corporate bonds, Asian debt and inflation-linked bonds provide interesting opportunities

While the worst of the recession is behind us, returning to the pre-coronavirus growth trajectory could take years

The global economy has recovered from the depths of the Covid-19 recession even as some countries grapple with new infections and lockdowns. Investors may want to seek out new sources of return potential that could benefit from the evolving recovery story – in addition to sectors that have prospered through the crisis.

Much depends on the successful deployment of an effective vaccine and drug therapies. New vaccines appear to hold promise, but we will be watching key macroeconomic data points for signs of momentum – and we expect wide differences in how regions perform. If the coronavirus is contained, attractive areas may include European and Asian equities, value sectors and corporate bonds. For institutional investors, private markets offer potential – infrastructure in particular could see increased spending, thanks in part to stimulus measures meant to boost economic activity. There are also an increasing number of opportunities to support a sustainable, resilient recovery of the post-coronavirus economy in ways that address climate change and other vital issues.

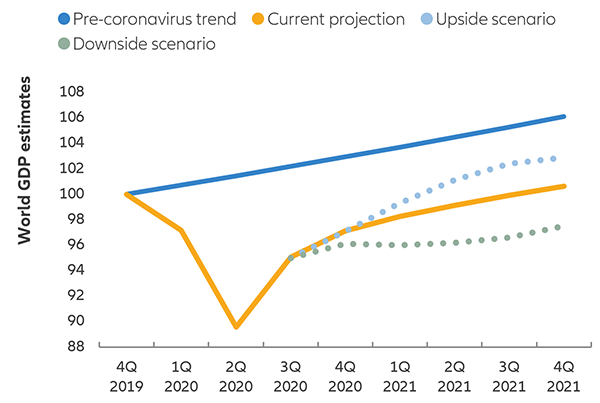

But if the pandemic is not brought under control, economic activity seems likely to reach pre-coronavirus levels only by the end of 2021. Economies might not return to their pre-coronavirus trend path for several years. This uncertainty is reflected in the OECD’s unusually wide range of growth forecasts (see Exhibit 1), with scenarios for 2021 varying from 7% to -2%.

Exhibit 1: this recovery isn’t V-shaped – it’s likely closer to a reverse square root sign

World GDP estimates (quarterly since 2019, indexed to 100)

Source: Allianz Global Investors, OECD. Data as at September 2020.

Countries have used stimulus to fight the coronavirus – but there may be economic casualties in the long term

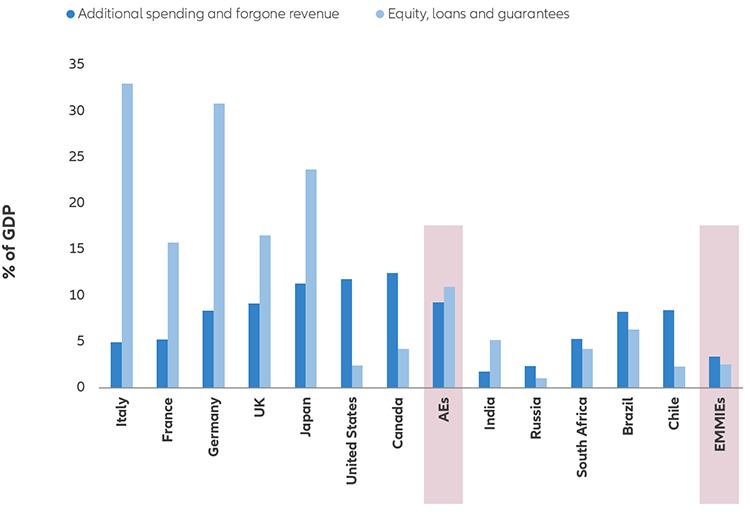

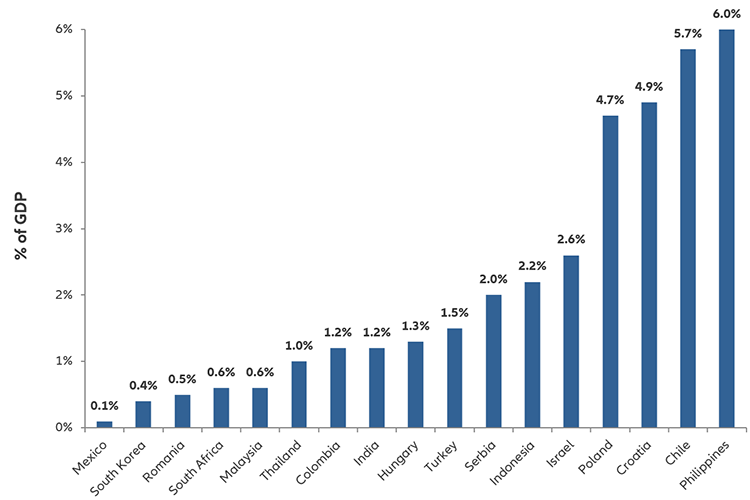

In response to the recent recession, governments and central banks provided vast amounts of monetary-policy stimulus and fiscal stimulus (see Exhibit 2). But although this support was necessary and helpful, it may also result in painful long-term side effects that include:

- High asset prices in some markets. Excess liquidity from monetary stimulus (essentially, too much money in circulation relative to economic activity) lifted asset prices – even some that already appeared overvalued. We think this is particularly true with government bonds and US equities, while non-US equities appear more moderately priced.

- High leverage. Public and private debt levels are elevated. If the recovery weakens significantly, companies might struggle to maintain their debt burdens – raising the risk of defaults. In addition, weak companies that renew cheap bank loans can turn into “zombie companies” – businesses with low productivity, high debt and a high risk of default if rates normalise.

- Rising inflation volatility. Risks are mounting that the prices for goods and services will grind higher in the medium term due in part to the excess liquidity from monetary stimulus, but also due to supply-side shocks related to the coronavirus shutdowns and ongoing trade wars. A continuation of the deglobalisation trend – as countries seek to be self-sufficient with essential goods – would be a drag on long-term economic growth and, consequently, on productivity growth. All else being equal, this could point to higher price volatility globally in the coming years.

Exhibit 2: massive discretionary fiscal response to the Covid-19 crisis

Announced measures in percent of GDP

Source: IMF Fiscal Monitor. Data as at September 2020. Country group averages are weighted by GDP in US dollars adjusted by purchasing power parity. AEs = advanced economies, which includes Italy, France, Germany, the UK, Japan, the US and Canada, plus other advanced economies as defined by the IMF. EMMIEs = emerging market and middle-income economies; this group includes India, Russia, South Africa, Brazil and Chile, as well as other emerging economies as defined by the IMF.

Download our global view and key themes

Download our asset class views

1390008

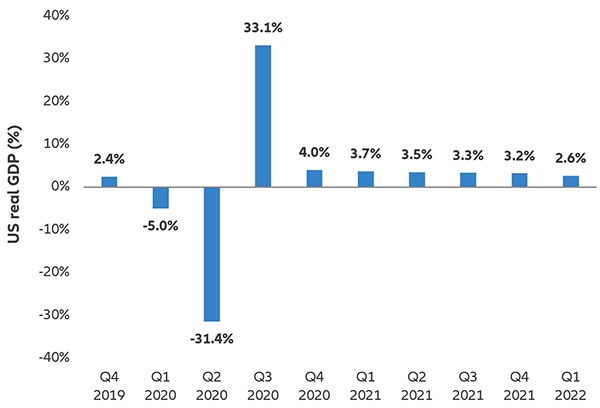

After a historic rebound in economic activity in the third quarter of 2020, the US growth outlook grew more moderate (see Exhibit 6). We expect this trend to continue throughout 2021, albeit with some surges and dips. Growth will likely still be above potential – meaning overall demand may outpace supply due to strong employment, high government expenditures and other factors – which may eventually spark inflation. Where the US economy ultimately ends up will likely depend on a few factors:

- The path of the virus will be a key determinant of consumer behaviour and economic activity. If new vaccines turn out to be as effective as promised, and if they are widely adopted, we expect to see strong growth.

- Until activity returns to pre-crisis levels, ongoing monetary and fiscal stimulus is critical for shoring up the economy in general, and small businesses in particular. Even so, we expect to see a rise in insolvencies among individuals and corporations unable to meet their financial obligations.

- The election of Joe Biden as the 46th US president will likely lead to new economic policies and more fiscal stimulus. The Biden administration's renewed focus on infrastructure spending and initiatives related to climate change and clean energy could create new opportunities for investors, including in the private markets space.

If US economic activity gradually returns to where it was before the coronavirus crisis hit, it may set up a generally benign backdrop for US risk assets such as equities and non-government bonds – though it will be important to choose carefully. In the case of another slowdown, markets will likely anticipate more fiscal and monetary stimulus – which could be supportive for risk assets as well. Either way, we may see a shift in which sectors are leading, and we expect market participation to broaden – meaning different sectors of the market may begin to outperform.

Exhibit 6: US growth will likely become more moderate as 2021 marches on

US real GDP forecast (quarter-over-quarter seasonally adjusted annual rate, in %)

Source: Bloomberg. Data as at October 2020.

In the European Union, the Covid-19 pandemic is being battled by 27 different member states. This makes the path of containment, the reaction of market participants and the speed of any rebound very difficult to predict. Continued lockdowns and social distancing would have a particularly strong impact on the service sector, and we would likely see insolvencies rise and employment fall across the EU. The markets would anticipate some uptick in insolvencies; what matters is whether they rise beyond expectations. We also assume that fiscal and monetary policy measures will help preserve the region’s economic fabric and avoid large-scale bankruptcies and layoffs.

The 19 countries in the euro zone carry the greatest weight – particularly Germany, France, Italy, Spain, the Netherlands, Belgium and Austria, which account for around 90% of the euro zone’s aggregated GDP. Overall, we expect the euro zone to grow by around 5.5% in 2021 after a projected collapse of 7.7% in 2020. This will be helped by several factors:

- Private consumption will probably profit from targeted government measures, an expected normalisation of current excess savings and a rebound in consumer confidence. We have a generally positive base-case view of consumer behaviour, but it may take time to normalise. It’s also unclear how consumers will react to continued coronavirus-related uncertainty, or how mass vaccinations may play out.

- Government consumption should help stem the economic fallout. A massive spending initiative such as the EUR 750 billion Recovery and Resilience Facility is an important milestone in addressing the crisis and a promising sign of European solidarity.

- Despite the uncertain outlook for domestic and external demand, we expect investment activity to pick up in 2021. The strain on company profit margins is likely to diminish and capacity utilisation is expected to rise.

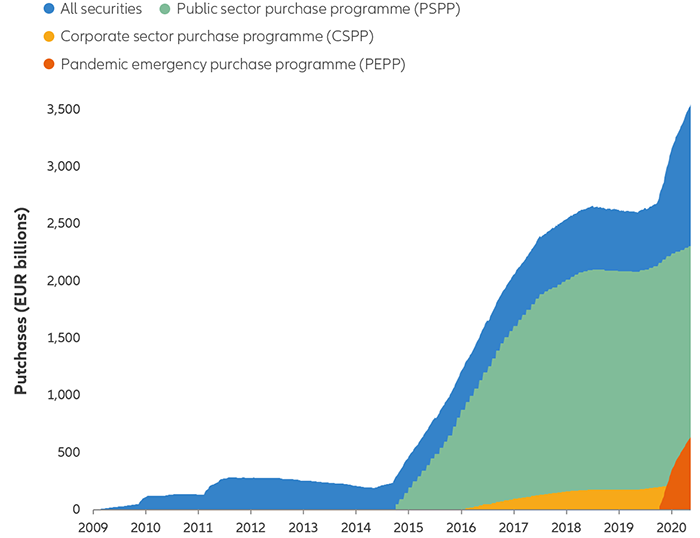

The inflation outlook remains relaxed for the time being, with euro-zone headline inflation expected to accelerate to a still-moderate 1.3% in 2021, up from 0.4% in 2020. Higher food and oil prices will exert a gradual upward push. Against this backdrop, the European Central Bank will likely stick to its extremely expansionary policy stance of low interest rates and continued asset purchases (see Exhibit 7). Within fixed income, we continue to prefer bonds in the euro-zone periphery, including Italy and Spain, over German government bonds. We also have a positive view of investment-grade corporate bonds. Both segments benefit from ECB purchase programmes.

We have a constructive outlook for European equities over the long term, thanks to their moderate valuations and our expectation that today’s promising vaccines, if broadly adopted, will help contain the virus’s spread.

Exhibit 7: the ECB’s balance sheet shows no sign of shrinking

ECB balance sheet, including key asset-purchase programmes (2009-2020)

Source: European Central Bank. Data as at November 2020.

Like the ECB, the Bank of England is planning to continue its bond-buying programme and keep interest rates low. The BoE is even contemplating a move into negative interest-rate territory. The UK economy has been in a difficult position as it grapples with the coronavirus and post-Brexit trade negotiations with the EU. As a result, significant uncertainty surrounds the pace and path of the recovery that started in May 2020. GDP is predicted to shrink 10%-12% in 2020, but given that we expect to see some success in containing the virus as well as the likely implementation of a UK-EU trade deal, we expect the UK to return to growth in 2021. Among the bright spots:

- Hard-hit sectors such as hotels, food service, transport, leisure and arts are set to benefit from a low starting point, boosting annual growth rates.

- Driven by the acceleration of e-commerce, the logistics sector is expected to expand forcefully.

- The construction sector should profit from fiscal measures to boost infrastructure investment.

All in all, we believe the UK economy will return to its pre-lockdown levels by the end of 2021, but our expectations could move significantly lower depending on the length and depth of the Covid-19 pandemic. We expect inflation to reach 1.6% in 2021, up from 1% in 2020, as energy prices normalise, the temporary VAT reduction fades and subdued wage growth picks up again. The UK’s budget deficit is projected to fall to nearly 7% in 2021 – down significantly from 2020 levels – but there could be additional fiscal stimulus measures to boost the economy. Still, once the economy recovers fully, fiscal spending needs to be reined in over the longer term to shrink public debt levels. The BoE is expected to stay the course with its expansionary monetary policy, including low to negative interest rates and asset purchases – though there is a possibility BoE policy could grow even more expansive depending on how the economy responds.

Given the UK’s challenges, we expect higher short-term volatility. This would emphasise the importance of taking an active investment approach in UK bonds as well as UK equities, which are relatively highly exposed to international developments. However, positive signals in the fight against the coronavirus and a UK-EU free trade agreement (instead of a “no-deal” scenario) would likely be buying opportunities.

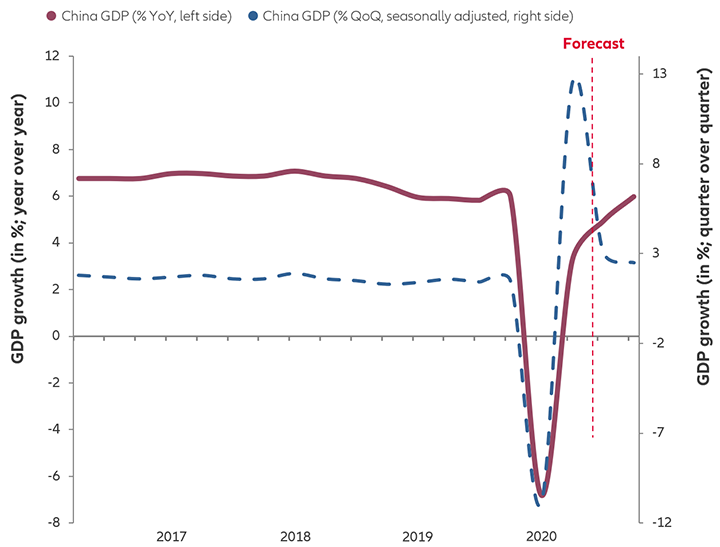

We expect China’s economy to keep up its strong recovery from Covid-19, which had a hugely negative impact early in 2020 even though the authorities quickly got the pandemic under control. Year-on-year GDP growth could be impressive in the early part of 2021 – in large part because the same period in 2020 was so deeply depressed (see Exhibit 8) – before slowing somewhat through the rest of the year.

China’s service sector seems set to continue its upward climb, assuming the government can suppress renewed outbreaks of the coronavirus. The manufacturing sector also seems likely to keep growing, helped by public investment projects and a gradual recovery of global demand as Covid-19 passes. And China is still positioning itself to win over the long-term by nurturing its own high-tech industries – particularly in the fields of robotics, aviation and other advanced-manufacturing areas.

We think this environment will lead China’s authorities to continue normalising the fiscal and monetary stimulus they provided in 2020. This means the government may start spending less, and the People’s Bank of China (PBoC) seems unlikely to make any major monetary easing moves – including rate cuts – in 2021. On the contrary, we could even see the PBoC start to tighten towards the end of the year if growth returns and core inflation picks up.

We are somewhat cautious on China’s investment outlook in the near term, given that fiscal and monetary policy are on a path of being normalised against an improving macroeconomic backdrop. Over the long term, however, China’s economic story is a compelling one. We think investors should continue to think of China as an asset class in and of itself – meaning it’s not so much a question of whether to invest in China, but how much to invest.

Exhibit 8: China’s GDP rebounded sharply in 2020, though it was still weaker than expected

Quarter-over-quarter and year-over-year GDP growth (actual through September 2020; estimated through December 2020)

Source: Bloomberg, CEIC, Allianz Global Investors. Data as at September 2020.

Emerging economies generally rebounded sharply after substantial losses in March 2020 – in large part thanks to extremely accommodative support from central banks (see Exhibit 9). Over the long term, we may see this support contribute to higher inflation globally. In the short run, however, we expect that factors such as weaker commodity prices will likely help avoid meaningful inflation pressures in the developing world. This will allow their central banks to cut rates to record low levels and experiment with some forms of asset purchase programmes (known as “quantitative easing”).

Exhibit 9: emerging-market central banks bought massive amounts of bonds to fight the effects of the coronavirus

Government-bond purchases by emerging-market central banks (March-October 2020)

Source: Bloomberg, IMF, Allianz Global Investors. Data as at October 2020.

But the massive amount of monetary and fiscal stimulus measures at work in emerging economies won’t last forever. For example, there is a limit to how low interest rates may go, given concerns about inflation, exchange rates and financial stability. Indeed, Turkey and Hungary already increased their policy rates in 2020. And fiscal stimulus measures – including increased spending – may soon become simultaneously less effective and increasingly scrutinised as investors assess whether too much spending hurts creditworthiness.

In the immediate future, Covid-19 continues to be the main risk for emerging-market growth. As viable vaccines become available, economic conditions around the world could normalise – which would help emerging and developed nations alike. But rising infection rates pose significant risk to vulnerable nations that have already spent much of their ammunition fighting the disease. As a result, we expect the recovery in emerging markets to be both fragile and diverse:

- While China and parts of Asia were the hardest hit by the pandemic initially, they were also the first to recover. Despite lingering concerns about second-wave infections that could pose a risk to the recovery, Asia saw a remarkable rebound in output when restrictive measures were lifted and factories resumed production. While this momentum may fade in 2021, governments throughout Asia will be providing fiscal support – and we expect this will help boost private consumption. Equities, credit and currencies appear attractive given our expectation that China and the rest of Asia will continue to bounce back.

- The CEEMEA region (Central and Eastern Europe, the Middle East and Africa) was off to a good start with its Covid-19 recovery until a spike in new cases. Poland could be a bright spot, thanks to its sizeable fiscal stimulus measures and closer integration with the European Union, while momentum in South Africa was already weak in the pre-Covid period. Similarly, the recovery in Russia was slower in part because of the oil industry, which reduced its output in recent negotiations with OPEC.

- Latin America was hit extremely hard by the pandemic, despite higher commodity demand from China and other countries helping the region’s commodity producers. Here, too, the recovery story is diverse. Brazil’s economy is vulnerable, whereas Mexico may recover steadily thanks to a rebound in US demand and manufacturing.

Overall, some emerging economies could enjoy robust quarterly GDP growth rates in 2021 given how low they were in the spring of 2020. But in many nations, economic activity is still below pre-Covid levels even as other challenges persist – from increased geopolitical tensions to broken supply chains and higher protectionism. However, with core emerging-market central banks signalling that their accommodative policies will not be reversed anytime soon, and with multilateral support ramping up from developed nations, emerging economies should feel external financial pressures ease somewhat.

Among emerging-market sovereign bonds, investors may want to consider high-yield over investment-grade securities, in part thanks to the external support the Fed and IMF are providing to developing nations.

In emerging Asia, fiscal and monetary support – along with positive developments in the fight against coronavirus – should help fuel the appetite for yield and risk assets. Across the region, we generally prefer fixed-income investments with shorter durations, and generally favour high-yield over investment-grade securities. In addition, a challenging environment for the US dollar could help India, Indonesia, the Philippines and other economies in South and South-East Asia. A weaker dollar means these countries’ central banks may not need to raise rates to help their currencies. It also makes it cheaper to hold debt denominated in US dollars and could result in more foreign inflows into the region.

We expect Japan’s real GDP to contract 5.5% in 2020 before recovering to 2.3% growth in 2021. Yet despite this rebound, the economic outlook remains uncertain. Households are likely to maintain a high savings rate and Japan’s exports are highly correlated with global capital expenditures, which are likely to wane given coronavirus-related uncertainty.

Prime Minister Yoshihide Suga is likely to continue pushing forward “Abenomics” – the economic policies of previous Prime Minister Shinzo Abe – particularly the combination of fiscal stimulus and large-scale monetary easing. Mr Suga has also emphasised the importance of maintaining a close relationship with the Bank of Japan (BOJ) and promoting additional monetary easing measures if they are deemed necessary to sustain employment and keep companies afloat. But for now, we think the BoJ is unlikely to lower its short-term policy rate further into negative territory.

Equities

The wide adoption of promising Covid-19 vaccines could benefit a range of regions and sectors – beyond the mega-cap US tech firms that have already done well. Likewise, a further deterioration on the Covid front is likely to put pressure on the direction of equity prices. So far, the growth outlook remains unclear and private-sector spending could be suppressed, which will place a greater burden on governments and central banks to provide stimulus. If virus-related fears about economic growth intensify, we expect that the financial markets will expect more stimulus – and begin to price it in.

Yet even now, central banks around the world are continuing to pump liquidity into their economies and trying to encourage investors to move out of “safe” assets and into riskier ones. This has stretched some equity valuations. For example, US equities not only constitute more than 50% of the global equity market in terms of market value, but also appear pricey when judged by most valuation metrics (including price-to-earnings ratios). However, we expect broader participation in the market’s performance in 2021:

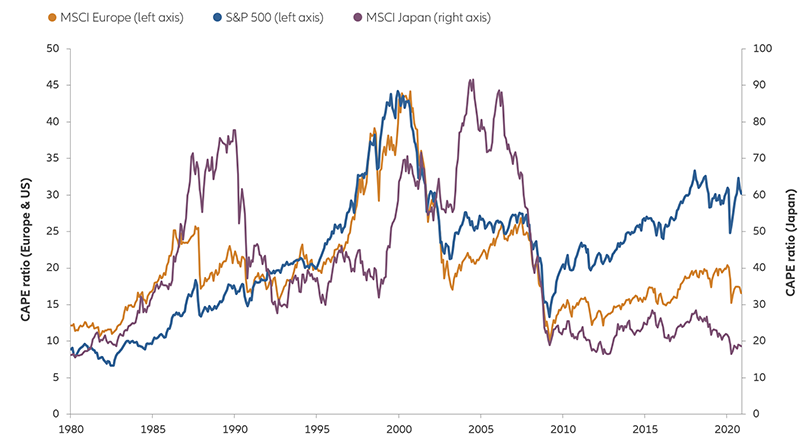

- As Exhibit 10 shows, some undervalued regions outside of the US could do well, particularly if we see a global rebound in growth. Look to Europe and emerging markets for potential value cyclical opportunities.

- Consider North Asia and China for secular growth themes, such as China’s investment in new infrastructure and the overall shift towards digitalisation in Asia – including e-commerce, 5G and artificial intelligence.

- The outlook for emerging-market equities is diverse. For example, Poland and Mexico seem to have strong near-term prospects while Russia and Brazil are struggling – though they could be set to rebound when capital begins flowing back in.

- The value style of investing has underperformed and recently sold at a deep discount compared to its growth counterparts, so value cyclicals (including select industrials and financials) could benefit from the global economy’s continued re-opening.

- Under a Biden administration, clean energy sources – such as wind and solar – would likely benefit from increased investment and favourable tax and regulatory policies. Mr Biden has also indicated his support for investing in traditional infrastructure – such as the rebuilding of roads, bridges and airports – as well as technology infrastructure such as 5G and artificial intelligence.

Exhibit 10: equities in the US are expensive compared with Europe and Japan

Cyclically adjusted price/earnings ratios (1980-2020)

Fixed income

We believe there are attractive opportunities within the fixed-income markets, despite weak macroeconomic fundamentals. Abundant central-bank liquidity continues to provide a favourable backdrop for fixed-income securities in general, and particularly risk assets. As global economic growth recovers, we favour a reflation theme. This may take the form of US “curve steepener” trades (favouring short-term over long-term Treasuries; see Exhibit 11) and allocating risk to spread products (including emerging-market debt, investment-grade corporate bonds and high-yield debt). Another argument in favour of these areas is that central banks – which are price-insensitive buyers of bonds – participate in some of these markets. We are fully aware of the fact that leverage in the corporate sector has significantly increased during this recession. With the US dollar potentially set to fall in value, investors may want to consider underweighting the currency.

The speed and scale of the monetary and fiscal policy measures related to the pandemic have helped reduce the depth and longevity of the global recession, and the global economy has started to recover. But as governments in the developed world continue to provide large-scale stimulus to support their economies, there has been a significant deterioration in government-debt metrics. We believe this means central-bank policy will be generous for the foreseeable future, just as we saw after the 2008-2009 financial crisis. Policy makers want to keep interest rates low to support the recovery; they don’t want to raise rates and risk triggering defaults. Expect to see continued monetary accommodation – including quantitative easing and interest rates that hover near zero (or even move into negative territory) – as policymakers navigate the new macroeconomic landscape.

Exhibit 11: the US yield curve has started to steepen

5-year/30-year Treasury spread (2010-2020)

Private markets

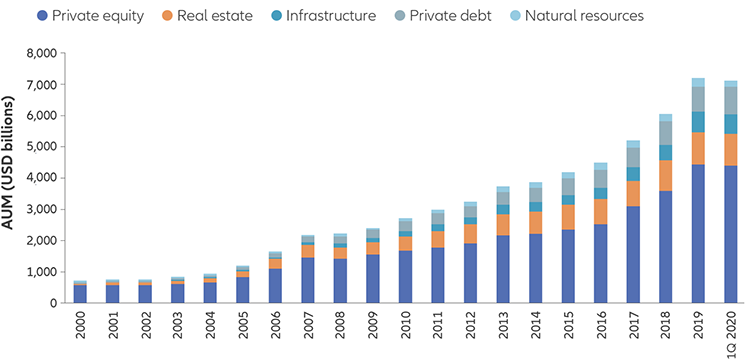

Private markets have enjoyed significant growth in recent decades (see Exhibit 12), in large part because of their ability to provide institutional investors with the potential for excess returns and alternative revenue sources that are largely uncorrelated to public markets. Market dynamics have also been favourable to this asset class. Growing regulatory challenges have put pressure on banks, creating an opportunity for institutional investors to provide capital, and in recent years there has been increased activity from corporations ready to put these funds to work. With growth in average deal values, more companies can rely on funding from investors and stay private for longer.

From the outset, the Covid-19 pandemic quickly created stress and uncertainty in markets around the world. As economic activity slowed, many businesses were forced to react to the situation by cutting costs and capital expenditures, and by drawing on credit lines. Governments responded by committing vast sums for emergency financing while banks mainly concentrated on key relationships and core sectors. However, with bank and credit insurer activity expected to tighten, we foresee a growing demand for credit from mid-market corporations and non-core infrastructure sectors – as well as a greater demand for trade finance across all sectors of the economy. Institutional investors can benefit from this development and capture opportunities through private-market investments – and in turn help finance the recovery of the real economy.

Asia is one example of the opportunity available to private-market investors. In a world where growth is in short supply, Asia has a bright outlook for growth thanks to its rising middle class, increasing consumption, strong productivity and rapid pace of digitisation. Moreover, most Asian governments have responded to the Covid-19 crisis by boosting fiscal and infrastructure spending – further fuelling many of these trends. Middle-market companies in Asia stand to be among the primary beneficiaries of these growth drivers, yet many of these firms lack credit. Investors have an opportunity to provide funding to these companies through the private credit markets. This gives investors access to attractive risk-adjusted return potential, proprietary cash flows, and limited correlation to broader fixed-income and equity markets through real assets – as opposed to financial assets.

It is true that globally, some sectors have struggled during this crisis – particularly airports, retail and construction. Yet others that provide essential services to the public have seen a very limited impact on demand (including telecom towers, pharmaceuticals, regulated utilities and data centres) or are expected to experience a sharp rebound (such as healthcare, transport, education and business software) as economies recover. Across multiple sectors, private markets have demonstrated their resilience and ability to add value in an institutional portfolio context – including exhibiting rating volatility that has generally been far lower than the public markets have experienced.

The pace of deal activity seems to have regained steam after a slowdown in the first half of 2020. With governments launching new stimulus packages to help support their economies, institutional investors can play a vital role in the post-pandemic recovery. Given the macro environment, we expect a larger set of investment opportunities to emerge while valuation expectations and credit terms return to more reasonable levels.

Exhibit 12: private markets have grown exponentially in the last 20 years

Assets under management (2000-2020)

Source: Preqin. Data as at March 2020.

Download our global view and key themes

Download our asset class views

1390008

-

The MSCI World Index is an unmanaged index considered representative of stocks of developed countries. The MSCI All Country World Index (ACWI) is an unmanaged index designed to represent performance of large- and mid-cap stocks across 23 developed and 24 emerging markets. The MSCI Europe Index is an unmanaged index that measures the performance of the equity market of the developed markets in Europe. The MSCI Japan Index is an unmanaged index that measures the performance of the equity market of Japan. The Standard & Poor’s 500 Composite Index (S&P 500) is an unmanaged index that is generally representative of the US stock market. Investors cannot invest directly in an index.

Investing involves risk. The value of an investment and the income from it will fluctuate and investors may not get back the principal invested. Equities have tended to be volatile, and do not offer a fixed rate of return. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bond prices will normally decline as interest rates rise. The impact may be greater with longer-duration bonds. Credit risk reflects the issuer’s ability to make timely payments of interest or principal—the lower the rating, the higher the risk of default. Emerging markets may be more volatile, less liquid, less transparent, and subject to less oversight, and values may fluctuate with currency exchange rates. Investments in alternative assets presents the opportunity for significant losses including losses which exceed the initial amount invested. Some investments in alternative assets have experienced periods of extreme volatility and in general, are not suitable for all investors. Environmental, Social and Governance (ESG) strategies consider factors beyond traditional financial information to select securities or eliminate exposure which could result in relative investment performance deviating from other strategies or broad market benchmarks. Past performance is not indicative of future performance. This is a marketing communication. It is for informational purposes only. This document does not constitute investment advice or a recommendation to buy, sell or hold any security and shall not be deemed an offer to sell or a solicitation of an offer to buy any security.

The views and opinions expressed herein, which are subject to change without notice, are those of the issuer or its affiliated companies at the time of publication. Certain data used are derived from various sources believed to be reliable, but the accuracy or completeness of the data is not guaranteed and no liability is assumed for any direct or consequential losses arising from their use. The duplication, publication, extraction or transmission of the contents, irrespective of the form, is not permitted.

This material has not been reviewed by any regulatory authorities. In mainland China, it is used only as supporting material to the offshore investment products offered by commercial banks under the Qualified Domestic Institutional Investors scheme pursuant to applicable rules and regulations. This document does not constitute a public offer by virtue of Act Number 26.831 of the Argentine Republic and General Resolution No. 622/2013 of the NSC. This communication's sole purpose is to inform and does not under any circumstance constitute promotion or publicity of Allianz Global Investors products and/or services in Colombia or to Colombian residents pursuant to part 4 of Decree 2555 of 2010. This communication does not in any way aim to directly or indirectly initiate the purchase of a product or the provision of a service offered by Allianz Global Investors. Via reception of his document, each resident in Colombia acknowledges and accepts to have contacted Allianz Global Investors via their own initiative and that the communication under no circumstances does not arise from any promotional or marketing activities carried out by Allianz Global Investors. Colombian residents accept that accessing any type of social network page of Allianz Global Investors is done under their own responsibility and initiative and are aware that they may access specific information on the products and services of Allianz Global Investors. This communication is strictly private and confidential and may not be reproduced. This communication does not constitute a public offer of securities in Colombia pursuant to the public offer regulation set forth in Decree 2555 of 2010. This communication and the information provided herein should not be considered a solicitation or an offer by Allianz Global Investors or its affiliates to provide any financial products in Brazil, Panama, Peru, and Uruguay. In Australia, this material is presented by Allianz Global Investors Asia Pacific Limited (“AllianzGI AP”) and is intended for the use of investment consultants and other institutional/professional investors only, and is not directed to the public or individual retail investors. AllianzGI AP is not licensed to provide financial services to retail clients in Australia. AllianzGI AP (Australian Registered Body Number 160 464 200) is exempt from the requirement to hold an Australian Foreign Financial Service License under the Corporations Act 2001 (Cth) pursuant to ASIC Class Order (CO 03/1103) with respect to the provision of financial services to wholesale clients only. AllianzGI AP is licensed and regulated by Hong Kong Securities and Futures Commission under Hong Kong laws, which differ from Australian laws.

This document is being distributed by the following Allianz Global Investors companies: Allianz Global Investors U.S. LLC, an investment adviser registered with the U.S. Securities and Exchange Commission; Allianz Global Investors Distributors LLC, distributor registered with FINRA, is affiliated with Allianz Global Investors U.S. LLC; Allianz Global Investors GmbH, an investment company in Germany, authorized by the German Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin); Allianz Global Investors (Schweiz) AG; Allianz Global Investors Asia Pacific Ltd., licensed by the Hong Kong Securities and Futures Commission; Allianz Global Investors Singapore Ltd., regulated by the Monetary Authority of Singapore [Company Registration No. 199907169Z]; Allianz Global Investors Japan Co., Ltd., registered in Japan as a Financial Instruments Business Operator [Registered No. The Director of Kanto Local Finance Bureau (Financial Instruments Business Operator), No. 424, Member of Japan Investment Advisers Association and Investment Trust Association, Japan]; and Allianz Global Investors Taiwan Ltd., licensed by Financial Supervisory Commission in Taiwan.

Financial repression “reloaded” and massive government debt could drive up long-term yields

Given the support that central banks pledged in the face of Covid-19, we expect short-term interest rates to remain at ultra-low levels for the foreseeable future. This is essentially a “reloading” of the financial-repression policies (including low interest rates, restricted capital flows and other regulations) that central banks implemented after the financial crisis to help their economies grow their way out of debt. In our view, continued intervention by central banks is necessary, but it could still lead to higher inflation and other problems in the medium to longer term. In addition, a huge supply of sovereign bonds – the direct consequence of extremely expansionary fiscal policy – will continue to flood the bond markets in the coming quarters.

What does it mean for investors?

Equities could benefit from positive news about the coronavirus – but balance and selection are key

Amid the upheaval of the Covid-19 pandemic and accompanying lockdowns, certain regions and asset classes did quite well – particularly US large-cap technology and online retail names that benefited from the “stay-at-home” trend. Positive developments in the fight against the coronavirus could help a broader range of stocks and regions in addition to these “coronavirus winners”.

One such positive development was the announcement of promising vaccine trials towards the end of 2020. Yet it remains unclear how long it will take to roll out these vaccines and how many people will be willing to get them. Until then, many regions will likely grapple with subsequent waves of coronavirus infections. So as we wait for effective vaccines and therapeutic treatments to be broadly adopted, the growth outlook will be unclear and private-sector spending (including private consumption and investments) could be suppressed.

If cyclical economic data lose momentum, equities could suffer – particularly if the markets see a disconnect between asset prices and the underlying health of the economy.

What does it mean for investors?

Exhibit 3: the value investing style is at an extreme discount to growth

Relative valuation of MSCI World Value/Growth (1985-2020)

Source: Refinitiv Datastream, Allianz Global Investors. Data as at October 2020.

The US dollar seems more likely to weaken, which would benefit non-US markets

As the global economic rebound ramped up, the US dollar fell in value relative to other currencies (see Exhibit 4). While some economists see a turnaround on the horizon – in large part because uncertainty about Covid-19 is supportive for “safe-haven” assets such as the US dollar – we are slightly more inclined to believe the dollar will fall for several reasons:

What does it mean for investors?

Exhibit 4: the US dollar dropped in 2020 as the global economy recovered

US dollar trade-weighted index (2015-2020)

Source: Bloomberg, Allianz Global Investors. Data as at October 2020.

Sustainable investing provides the long-term view investors need

The coronavirus pandemic exposed shared vulnerabilities in the global economy and the systems on which we all rely. Investors will increasingly need to find ways to be selective among sectors and individual names, rather than rely on broad market performance. Environmental, social and governance (ESG) factors can be a helpful lens for highlighting major global risks and testing the resilience of businesses and systems.

The Covid-19 pandemic also forced many investors to hit the “reset” button and recalibrate their priorities, with policymakers, regulators and investors examining the social effects of economic activity. A growing number of investors will want to put their capital to work in a sustainable way, and they’ll be looking for creative ideas to help achieve meaningful real-life change on topics such as climate change.

This may happen within the framework of the 17 UN Sustainable Development Goals (SDGs), which call for greater cooperation between countries, organisations, companies and individuals to address vital development issues. A 2017 UN report put the SDG funding gap in developing countries at around USD 2.5 trillion per year, making it critical to find innovative and scalable new investment products for the countries and sectors most deprived of funding. This can take the form of public/private partnerships, with parties with similar goals shouldering different responsibilities. The field of development finance – which uses capital and know-how from public and philanthropic sources to mobilise private investment into sustainable development – can play a crucial role here.

For example, given that massive spending is still needed to return parts of the economy to its pre-pandemic growth trajectory, some governments see an opportunity to rejuvenate existing infrastructure such as electricity networks. This can be done while building the social, environmental and clean-energy projects that will support the well-being and prosperity of future generations.

But sustainable investing is not just about doing good – it also helps investors seek solid performance. As Exhibit 5 shows, approximately two-thirds of active ESG managers in the eVestment database (which tracks institutional asset managers) have beaten the benchmark index for global equities during the last three years. This includes 2020 – an extremely volatile period for equities.

Exhibit 5: the majority of active global ESG managers have beaten the benchmark global equity index over the last 3 years

Percentage of active managers in eVestment Global Equity ESG database that outperformed the MSCI All Country World Index (through 3Q 2020)

Source: eVestment. Data as at September 2020. The bars represent the % of active managers in the eVestment Global ESG database outperforming the MSCI ACWI Index in each period.

What does it mean for investors?

There are many options for investors who want to put their money to work in a sustainable way – particularly as the world recovers from the Covid-19 pandemic.